Published on the 6th June 2023

What Does Travel Insurance NOT Cover?

Reading Time: 6 min read

Many adventurers take out travel insurance for peace of mind, and given the unpredictability of life, it makes any upcoming trip that much safer. Knowing precisely what you’re covered for is just as important as deciding where to get travel insurance and every policy has intricacies and exclusions. Let’s look at typical policies, and what travel insurance does not cover so you’re fully aware of the situation before investing.

Contents

- What Does Travel Insurance Not Cover

- What Does Travel Insurance cover?

I. Basic and standard coverage

II. Comprehensive coverage

-

Conclusion

What Does Travel Insurance Not Cover?

You should never assume that your travel insurance policy will over any unforeseen circumstances on your trip whether it be injury, illness or loss. The majority of travel insurance policies will compensate you for a variety of unexpected circumstances including baggage loss and some personal injury but you should expect that not all of potywntial scenarios will be covered by the most basic of policies.

When sourcing the right deal for your circumstances, pay particular attention to areas not covered by your policy. Many assume that their coverage extends beyond its actual remit, but all levels of coverage come with specific terms and conditions.

· Irresponsible baggage loss

As stated, baggage loss is covered by most minimal-coverage travel insurance companies. But companies are unlikely to pay out if such a loss is deemed the owner’s fault. If you leave your bag unattended or in the hands of a stranger, you won’t be covered if it goes missing.

· Hedonism

Likewise, if you suffer a personal injury whilst drunk or under the influence of a narcotic, the accident will likely be deemed to be your responsibility. It’s very unlikely that travel insurance will be paid out following an inebriated mishap.

· High-risk activities

Many choose a holiday to try something new for the first time like adventure sports, be it bungee jumping, mountain climbing, or swimming with sharks. Such dangerous activities may not be covered, even by comprehensive travel insurance. Try to decide what high-risk activities you’re going to be trying in advance of your trip, and discuss this with insurance representatives prior to agreeing on any deal.

· Natural disasters

Many policies will cover you for severe weather patterns that arise from nowhere. But should a storm or hurricane be known of in advance and labelled, the same policy may not cover you. For the best defence against such occurrences, take out a policy early – securing insurance in advance of a destructive weather pattern being named may mean you’re covered for it.

· Pregnancy

Pregnancy is on a par with personal health issues, and is not considered a sickness nor an illness. If a pregnant woman decides not to travel, a cancelled trip will not be covered.

· State regulations

Most states have a recommended list of places they deem unsafe for their citizens to visit. Most of these are long-term, but instability can happen at short notice, and a foreign paradise can turn into a place of unrest in no time at all.

If your government has placed your chosen destination on their ‘dangerous’ list, your insurance won’t cover any cancellation.

· Non-essential medical procedures

If the purpose of your trip abroad is to secure a particular medical procedure and something goes wrong, it’s unlikely that travel insurance will cover it. Medical tourism is a growing industry, given the much lower prices that can be found abroad in comparison to the West. Most travel insurance plans will only cover you for emergency medical care expenses arising out of accidents or illnesses.

What Does Travel Insurance Cover?

Travel plans fall into three levels of coverage – basic, standard, and comprehensive. The former is a cheaper insurance option and covers many of the basics, as we’ll see below.

1. Basic & standard coverage

The following list is not exhaustive, and in a competitive world, what one insurer deems ‘basic’ will be deemed ‘standard’ to another. However, a basic or standard policy should include some or all of the following:

· Responsible baggage loss

Does travel insurance cover your luggage? Usually, if an airline manages to displace your bag or if it’s ripped from your hands by a thief, you can file a successful claim for the cost of its contents. Different policies will cover you for different monetary amounts for lost or stolen luggage. Some may also insure you for temporary loss, such as an airline misplacing your bag, only to find it later.

· Death or personal injury

Minimum levels of insurance will cover most instances of personal injury and accidental death. They won’t pay out the same compensation as life insurance, which must be covered in a separate policy.

· Essential cancellations

Travel insurance coverage will typically cover you if you have to cancel a trip due to an emergency. All insurers have different rules, so be sure to read the small print. Essential reasons for cancellation may include natural disasters, personal or family member illness, and unemployment. Most minimum coverage will also cover you for holidays that have to be cut short, for similar reasons as those stated.

· Long delays

A ten-minute flight delay is unlikely to be included in a travel insurance policy, but one that eats significant time out of your holiday week or fortnight will usually be covered. Acceptable timescales will often differ from one policy to the next.

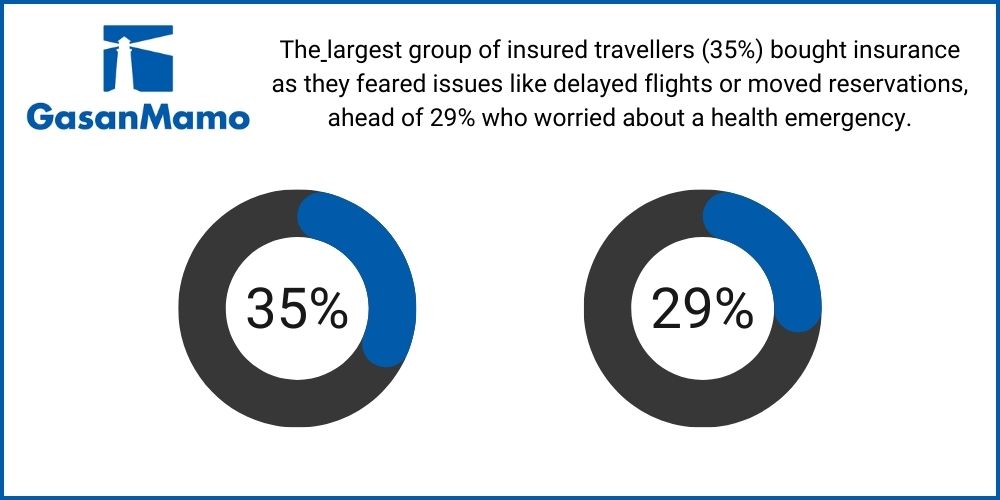

Interestingly, long delays are high on the list of priorities for those purchasing travel insurance coverage. A study showed that the largest group of insured travellers (35%) bought insurance primarily because they feared issues like delayed flights or moved reservations, ahead of 29% who worried about a health emergency.

2. Comprehensive coverage

Comprehensive coverage naturally includes the basic and standard facets detailed above, along with some or all of the following:

-

- Covid-19 coverage

The issue of Covid-19 can be a thorny one indeed when it comes to travel. We’ve recently seen certain governments ban all travellers, demand tests for entry, or require specific levels of insurance coverage. At the height of the pandemic, many travel insurers did not cover Covid-19, but at the time of writing, certain levels of coverage are available from most.

These may cover your medical expenses if you contact Covid-19 whilst abroad. Although the Covid-19 situation has improved worldwide as of 2023, it’s very much subject to change, so be sure to read advice for travellers and the intricacies of any insurance agreement before travel.

· Non-essential trip cancellation insurance

Travel insurance policies will cover you for cancellations beyond your control but not for a change of heart or non-essential reasons.

For further information, read our article on Why is travel insurance important?

Conclusion

Travel, health, and personal lifestyles can be complex things, so perhaps it’s no surprise that understanding trip insurance needs a little time and consideration. Knowing what travel insurance does not cover is just as essential as knowing what you’re covered for, so make sure any grey areas are clear before agreeing on a policy.

To get started, take a look at our competitive and comprehensive benefits, optional extras, and annual offer on our travel insurance page.